Budget 2024 was jam-packed with measures to support individuals and businesses tide over the challenging times, as well as invest in the future to better position themselves to take advantage of the opportunities of tomorrow.

Here is 24 key announcements that will have an impact on you and your financial well-being that you absolutely need to know about.

#1 Additional $600 in CDC Vouchers to be Given Out

Everyone’s favourite Community Development Council (CDC) Vouchers are back for yet another year!

First introduced in xxx, the scheme sees an enhancement in Budget 2024 with the distribution of an addition $600 in CDC Vouchers – the first tranche of $300 being given out in end-June 2024, followed by the remaining $300 being disbursed in January 2025.

Each tranche of CDC Vouchers will be split evenly between vouchers for spending at participating merchants/hawkers, and supermarkets.

#2 Increase in U-Save Credits

Singaporean HDB households whose members do not own more than one property will receive credits to offset their utilities’ bills in the months of April, July, October 2024 and January 2025. In total, this will amount to between $550 to $950 worth of offsets.

These credits are from the permanent GST Voucher (GSTV) Scheme, as well as additional credits from the previously announced Assurance Package (AP) and newly announced Budget 2024 Cost-of-Living (B2024 COL) measures.

| Flat Type and Disbursement Month | 1- and 2-room | 3-room | 4-room | 5-room | Executive/Multi-Gen |

| April 2024 | $190 | $170 | $150 | $130 | $110 |

| July 2024 | $285 | $255 | $225 | $195 | $165 |

| October 2024 | $190 | $170 | $150 | $130 | $110 |

| January 2025 | $285 | $255 | $225 | $195 | $165 |

| Total | $950 | $850 | $750 | $650 | $550 |

#3 Service and Conservancy Charges (S&CC) Rebates

Singaporeans HDB households will receive one-off rebates on their Service & Conservancy Charges (S&CC) bills which amounts to up to four months of S&CC rebates in FY2024.

Below is the disbursement months and amount of S&CC rebates based on HDB flat type.

| Flat Type and Disbursement Month | 1- and 2-room | 3- and 4-room | 5-room | Executive/ Multi-Gen |

| April 2024 | 1 | 1 | 0.5 | 0.5 |

| July 2024 | 1 | 0.5 | 0.5 | 0.5 |

| October 2024 | 1 | 0.5 | 0.5 | 0.5 |

| January 2025 | 1 | 1 | 1 | 0.5 |

| Total S&CC Rebates (in Months) | 4 | 3 | 2.5 | 2 |

#4 Cost-of-Living Special Payment

To help with the rise in cost-of-living, a one-off special cash payment will be made in September 2024 to eligible Singaporeans.

Recipients must be 21 and above in 2024, residing in Singapore, and do not own more than one property. The quantum of the payout will also depend on one’s Assessable Income (AI) in YA2023.

| AI of up to $22,000 | AI of more than $22,000 and up to $34,000 | AI of more than $34,000 and up to $100,000 | |

| COL Special Payout Quantum | $400 | $300 | $200 |

#5 Majulah Package – Earn-and-Save Bonus (ESB)

To encourage and incentivise Singaporean seniors to keep working, an Earn-and-Save Bonus (ESB) will be given to all Singaporeans born in 1973 or earlier who work and earn an average monthly income of between $500 and $6,000; live in a residence with Annual Value (AV) of $25,000 or below; and who do not own more than one property.

The ESB is given in the form of a direct top-up to the senior’s CPF Retirement Account (RA) or Special Account if the RA has not yet been created. The first annual ESB credit will be made in March 2025.

Eligibility for ESB will be assessed annual based on the preceding year’s property AV and income, and the quantum will be tiered based on average monthly income.

| Average Monthly Income | Annual Bonus |

| $500 to $2,500 | $1,000 |

| Above $2,500 to $3,500 | $700 |

| Above $3,500 to $6,000 | $400 |

Note that persons with disabilities, workers who qualify for ComCare Short-to-Medium Term Assistance and caregivers of care recipients will also qualify for concessionary ESB of $400 a year, even if they earn less than $500 a month.

#6 Majulah Package – Retirement Savings Bonus (RSB)

The Retirement Savings Bonus (RSB) is designed to support seniors with a small amount of retirement savings through top-up to the seniors’ CPF Retirement Account (RA) or Special Account if the RA has not yet been created.

To qualify for the RSB, you have to be a Singaporeans born in 1973 or earlier; live in a residence with Annual Value (AV) of $25,000 and below while not owning more than one property as at 31 December 2023; and have combined CPF LIFE and RA balances (or combined Ordinary Account and Special Account balances if the RA has not yet been created) of less than $99,400 as at 31 December 2022.

The quantum of RSB will be tiered by CPF retirement savings and will be credited in December 2024.

| CPF Retirement Savings | Bonus |

| Less than $60,000 | $1,500 |

| At least $60,000 but less than $99,400 (Basic Retirement Sum in 2023) | $1,000 |

#7 Majulah Package – MediSave Bonus (MSB)

All Singaporeans born in 1973 or earlier will receive this MediSave Bonus (MSB) which will be deposited in their CPF MediSave Account in December 2024.

For those born between 1960 to 1973; do not own more than one property; and reside in a property of Annual Value (AV) of not more than $25,000; they will receive $1,500. Otherwise, all other eligible Singaporeans will receive $750.

#8 One-Time MediSave Bonus (MSB)

Aside from the substantial MediSave Bonus given to seniors under the Majulah Package, the all adult Singaporeans between the ages 21 and 50 (born in 1974 – 2003) will also receive a one-time MediSave Bonus to offset healthcare costs and build up medical savings for old age.

This bonus will be credited to recipients’ CPF MediSave Account in December 2024 and is tiered by their year of birth, the Annual Value (AV) of their residence, and whether they own more than one property as at 31 December 2023.

| Singaporeans Born In | Own Not More Than 1 Property and AV of Residence Not More than $25,000 | Own More Than 1 Property or AV of Residence More than $25,000 |

| 1974-1983 | $300 | $200 |

| 1984-2003 | $200 | $100 |

#9 National Service (NS) LifeSG Credits

The National Service (NS) LifeSG credits are meant to recognize the contributions of past and present NSmen, including those enlisting by 31 December 2024. Eligible NSmen will be notified by SMS.

$200 in LifeSG credits will be disbursed by November 2024 and will be valid for one year from date of issue. Credits can be accessed through the LifeSG mobile application and spent at over 100,000 online and physical merchants that accept payments through PayNow UEN QR or NETS QR.

#10 ComLink+ Progress Package

During this year’s Budget, the ComLink+ Progress Package was introduced to recognise and support lower-income families with young children to achieve greater stability, self-reliance and social mobility in life.

To qualify for various financial top-ups under the package, families must reach pre-determined action plan milestones set by assigned family coaches from the Ministry of Social and Family Development. When they do so, they will be eligible for financial support such as top-ups to childrens’ Child Development Account (CDA), cash and CPF top-ups, matched debt repayments, and matched voluntary CPF contributions.

This package is introduced as a pilot scheme for three years, during which its effectiveness will be evaluated before any potential scale ups. Some of the financial incentives are funded by corporate and community donors.

#11 $4,000 SkillsFuture Credit (Mid-Career) Top-Up

This substantial SkillsFurture Credit (SFC) of $4,000 introduced at Budget 2024 will see every Singaporean receiving this top-up when they turn 40 years old. Those who are currently aged 40 and above will receive this top-up in May 2024.

These credits have no expiry date and can be used for selected industry-oriented courses to boost employability outcomes. More details will be announced in due course.

#12 Full Subsidies for Full-Time Second Diploma

From Academic Year (YA) 2025 onwards, Singaporeans aged 40 and above will be eligible for the Mid-Career Enhanced Subsidy to study for another subsidized full-time diploma at local Polytechnics, ITE and arts institutions like NAFA and LASALLE.

In the past, individuals who have received Ministry of Education subsidies or government sponsorships for a diploma or degree qualifications are not eligible for another subsidised full-time diploma qualification at local institutions.

#13 SkillsFuture Mid-Career Training Allowance

This new allowance scheme was introduced encourage and support mid-career workers who need to take a break from their careers to take up full-time long-form training opportunities, such as SkillsFuture Career Transition Programme courses or full-time publicly-funded full qualifications up to undergraduate level.

This allowance will partially offset the loss of income from work and be available for eligible learners aged 40 and above from early 2025. The allowance will be equivalent to 50% of their average income over the latest available 12-month period, capped at $3,000 a month. There is also a lifetime limit of receiving 24 months of training allowance per person.

#14 Enhancements to Workfare Income Supplement Scheme

In Budget 2024, the Workfare Income Supplement Scheme (Workfare) will be enhanced in two ways from 1 January 2025.

First, the qualifying wage cap will be raised from $2,500 to $3,000. This takes into account wage growth of Singaporeans and will enable more workers to benefit from the scheme.

Second, Workfare payments will be increase to up to $4,900 a year (up from a maximum of $4,200), although the actual amount will differ based on age band and income. Payments for self-employed persons remain set at two-thirds of what workers receive, and thus will be correspondingly increased.

| Age Band | Before Enhancement (Work Done Until 31 December 2024) | After Enhancement (Work Done From 1 January 2025) |

| 30 to 34 | $2,100 | $2,450 |

| 35 to 44 | $3,000 | $3,500 |

| 45 to 59 | $3,600 | $4,200 |

| 60 and above | $4,200 | $4,900 |

| All persons with disabilities | $4,200 | $4,900 |

#15 Introduction of New ITE Progression Award

To encourage young ITE graduates to not stop at their NITEC or Higher NITEC qualification, an ITE Progression Award was announced at Budget 2024.

Given to ITE graduates who pursue a diploma qualification, this award provides a $5,000 top-up to the learner’s Post-Secondary Education Account (PSEA) upon enrolment, and an additional $10,000 top-up to the learner’s CPF Ordinary Account upon graduation.

#16 Revision of Income Criteria for Healthcare and Associated Social Support Schemes

After taking into consideration changes in household incomes, as well as increased cost of healthcare and social support services, the income criteria for means-tested healthcare and associated social support subsidy schemes will be increased by 4Q 2024.

This revision will allow Singapore Citizens and Permanent Residents to benefit from higher subsidies, with higher subsidies extended to lower-income groups. A total of 13 schemes and services will be impacted by the revised income criteria:

- MediShield Life and CareShield Life Premium Subsidies;

- Community Health Assist Scheme (“CHAS”);

- Subsidies at Publicly-Funded Hospitals2;

- MOH and MSF Long-Term Care Residential and Non-Residential Services3,4;

- Community Haemodialysis and Peritoneal Dialysis Subsidies;

- Standard Drug List and Medication Assistance Fund Drugs;

- Seniors’ Mobility and Enabling Fund;

- Home Caregiving Grant;

- Interim Disability Assistance Scheme Programme for the Elderly;

- ElderFund;

- Enabling Transport Subsidy;

- Taxi Subsidy Scheme; and

- Assistive Technology Fund.

The monthly per capita household income (PCHI) threshold for each subsidy tier will be raised by between $100 to $800.

| Scheme | Monthly PCHI to Qualify for Maximum Subsidy | |

| Current | Revised | |

| MediShield Life and CareShield Life Premium Subsidies | ≤ $1,200 | ≤ $1,500 |

| CHAS | ||

| Specialist Outpatient Clinics | ||

| Standard Drug List | ≤ $2,000 | ≤ $2,300 |

| Acute Hospital | ≤ $1,800 | ≤ $2,100 |

| MOH and MSF Long-Term Care Residential & Non-Residential Services | ≤ $800 | ≤ $900 |

No action is required for patients and beneficiaries, as the respective service providers and scheme administrators will automatically extend the appropriate subsidies to those who are eligible when they use the services. CHAS cardholders who are eligible for a higher-tier CHAS card after the income criteria revision will be automatically issued with new CHAS cards.

#17 50% Personal Income Tax Rebate for YA2024 Capped at $200

There will be a personal income tax rebate of 50% of tax payable to all individual tax residents for the upcoming Year of Assessment 2024, capped at $200 per taxpayer.

There is no need to apply for this rebate, as the Inland Revenue Authority of Singapore (IRAS) will compute and grant the rebate automatically.

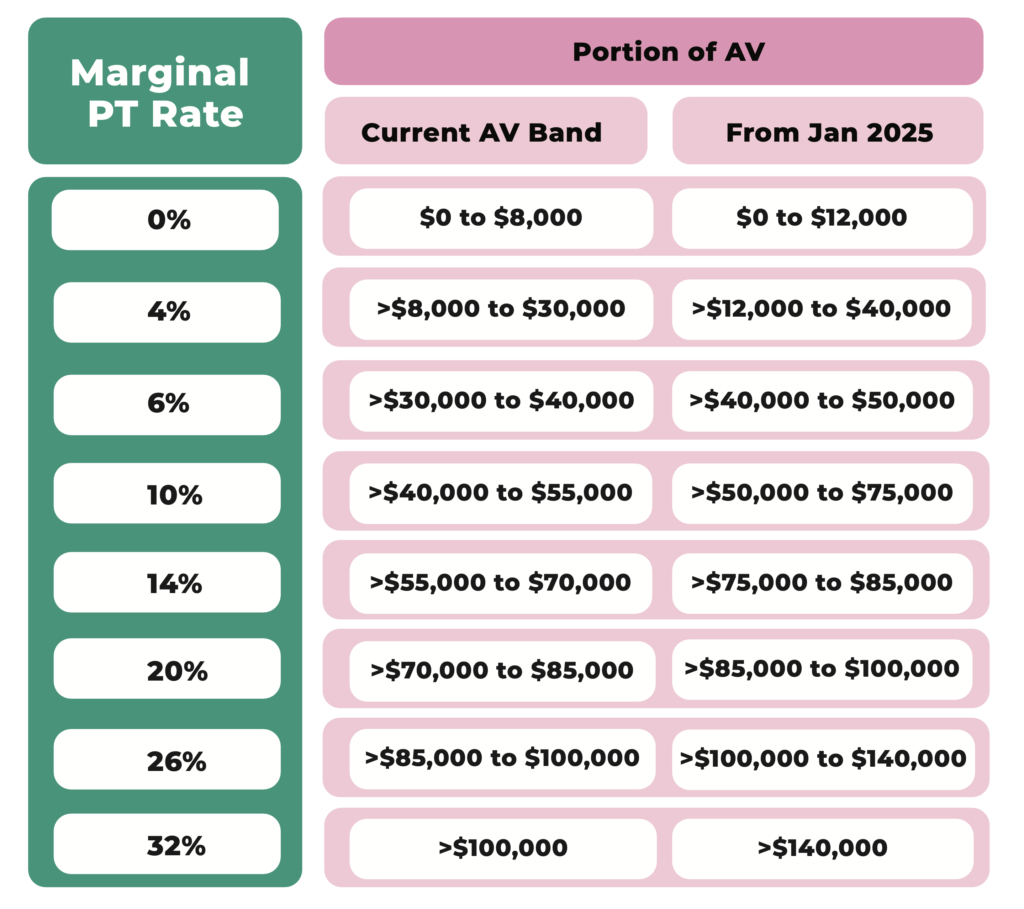

#18 Change to Property Tax Annual Value (AV) Bands

From 1 January 2025, the Annual Value (AV) bands for owner-occupied residential property tax will be revised. This takes into account the recent general steep rise in rental rates, and will result in homeowners paying the same or lower property taxes at each AV level.

#19 ABSD Concession for Single Retirees Who Are Downgrading

In the past, couples who dispose of their first residential property within six months of purchasing a second home are eligible for a refund of the Additional Buyer Stamp Duty (ABSD) they paid.

In Budget 2024, this concession will also be extended to single retirees aged 55 and above who are downgrading (right-sizing) to a smaller residential property. This applies to purchases on or after 16 February 2024, subject to them fulfilling all other relevant conditions.

#20 Enhancement to Silver Support Scheme (SSS)

The Silver Support Scheme (SSS) that supports Singaporeans aged 65 and above who had low incomes during their working years by providing cash payouts every quarter will be enhanced as part of Budget 2024.

From 1 January 2025, the criterion for monthly per capita household income (PHCI) will be raised from $1,800 to $2,300. The criteria for receiving higher SSS payout will also be raised from $1,300 to $1,500. This will enable more people to receive SSS payouts, and more people will be eligible for receiving higher SSS payouts.

In addition, the SSS quarterly payments will be increased by 20% across all payment tiers.

| HDB Flat Type | Current | From 1 January 2025 | ||

| Monthly PCHI of $1,300 or less | Monthly PCHI above $1,300 but not more than $1,800 | Monthly PCHI of $1,500 or less | Monthly PCHI above $1,500 but not more than $2,300 | |

| 1- and 2-room | $900 | $450 | $1,080 | $540 |

| 3-room | $720 | $360 | $860 | $430 |

| 4-room | $540 | $270 | $650 | $325 |

| 5-room | $360 | $180 | $430 | $215 |

There is no need to apply for SSS, since all Singaporeans aged 65 and above are automatically assessed for eligibility and notified by the CPF Board. All recipients of the enhanced SSS will receive their first payment in December 2024.

Note that Singaporeans aged 65 and above who are ComCare LTA beneficiaries also receive a SSS payment of $430 per quarter.

#21 Adjustment to Matched Retirement Savings Scheme (MRSS)

The Matched Retirement Savings Scheme (MRSS) encourages Singaporeans to contribute to the CPF Retirement Account (RA) of seniors’ (between the ages of 55 to 70) by providing dollar-for-dollar matching of up to $600 per year as well as tax reliefs.

From 1 January 2025, the government will expand the eligibility for this scheme and allow all seniors from the age of 55 to be eligible for MRSS. Furthermore, the yearly cap that is eligible for dollar-for-dollar matching from the government will be increased to $2,000 a year, subject to a lifetime cap of $20,000 per eligible member.

However, the tax relief that givers receive will be removed on cash top-ups that attract the MRSS matching grant. They would only receive tax relief of $16,000 a year for eligible CPF cash top-ups that do not attract the MRSS matching grant – such as $8,000 for cash top-ups made to their own SA, RA or MediSave Account, and another $8,000 for cash top-ups to similar accounts of their loved ones.

Other MRSS eligibility criteria still stands: the senior’s CPF RA savings (excluding interest earned and government grants, but inclusive of any amounts withdrawn) must be below the prevailing Basic Retirement Sum; the senior must also have an average monthly income of not more than $4,000; must not own more than one property; and whose Annual Value of residence is not more than $21,000.

The CPF Board will notify eligible members at the beginning of each year, though members can also check their eligibility through the CPF website. Members who receive a cash top-up within the year will receive the matching grant the following year.

#22 Continued Increase of Senior Workers CPF Contribution Rates

In Budget 2024, the government has moved yet another step towards its previously-stated goal of eventually making CPF contribution rates of workers aged above 55 to 70 the same as younger workers.

On 1 January 2025, CPF contribution rates for senior workers aged above 55 to 70 will be increased in the manner outlined in the table below, coming from both employers and employees.

| Age Band | Employer Contribution Rate (Percentage Point Change) | Employee Contribution Rate (Percentage Point Change) | Total Contribution Rate (Percentage Point Change) |

| 55 and Below | No Change | ||

| Above 55 to 60 | 15.5 (+0.5) | 17 (+1) | 32.5 (+1.5) |

| Above 60 to 65 | 12 (+0.5) | 11.5 (+1) | 23.5 (+1.5) |

| Above 65 to 70 | No Change | ||

| Above 70 | No Change | ||

For age bands that do not see any changes to contribution rates, this is because the target contribution rates had already been reached.

#23 Increase of Enhanced Retirement Sum (ERS) to Four Times the Basic Retirement Sum (BRS)

The CPF Enhanced Retirement Sum (ERS) controls the maximum amount of savings that CPF members aged 55 and above can deposit in their CPF Retirement Account – by way of cash top-ups or transfers from their CPF Ordinary Account) – which helps grows their retirement savings to eventually get higher CPF monthly payouts.

Currently, the ERS is set at three times the prevailing Basic Retirement Sum (BRS). From 1 January 2025, the ERS will be raised to four times the BRS.

| Year | BRS | ERS at 3 x BRS (Prior to 1 January 2025) | ERS at 4 x BRS (From 1 January 2025) |

| 2025 | $106,500 | $319,500 | $426,000 |

| 2026 | $110,200 | $330,600 | $440,800 |

| 2027 | $114,100 | $342,300 | $456,400 |

#24 Closure of CPF Special Account When Members Reach Age of 55

The government has announced at from early 2025, CPF members who reach the age of 55 and above will have their CPF Special Account (SA) closed. Their SA savings will be transferred to their Retirement Account, up to their cohort’s Full Retirement Sum, and any balance will then be transferred to their Ordinary Account (OA).

CPF members can then choose to transfer their OA savings to their RA, up to the Enhanced Retirement Sum, which has also been increased (see Section #23 Increase of Enhanced Retirement Sum (ERS) to Four Times the Basic Retirement Sum) in order to earn higher interest and eventually higher monthly CPF LIFE payouts.

The government has stated that the move is to better align CPF interest rates to the nature and liquidity of each CPF account. This will also stop the practice widely-referred to as “SA Shielding”.